How the best fund managers run the business behind the fund, not just the fund itself.

Ask a fund manager how the fund is doing and you will get an answer before you have finished the question. Returns, to the decimal. They know that number cold, because it is the number their investors care about and the number the next raise leans on.

So try a different question. How long can the business that runs the fund keep going once the fees start to shrink? When does the next fund need to launch to keep the team paid? That one tends to come back a lot slower.

That is the odd thing about a lot of fund managers. The fund itself gets measured to the last decimal. The business that runs it gets kept on the same basic books you would find at any small company. One gets all the attention. The other keeps the lights on, and nobody is really watching it. That second one is the part we find most interesting.

A fund manager is not a normal business

Most businesses earn, spend and grow in a fairly straight line. A fund manager does not. It runs on a cycle, and that cycle trips up ordinary bookkeeping.

It goes like this.

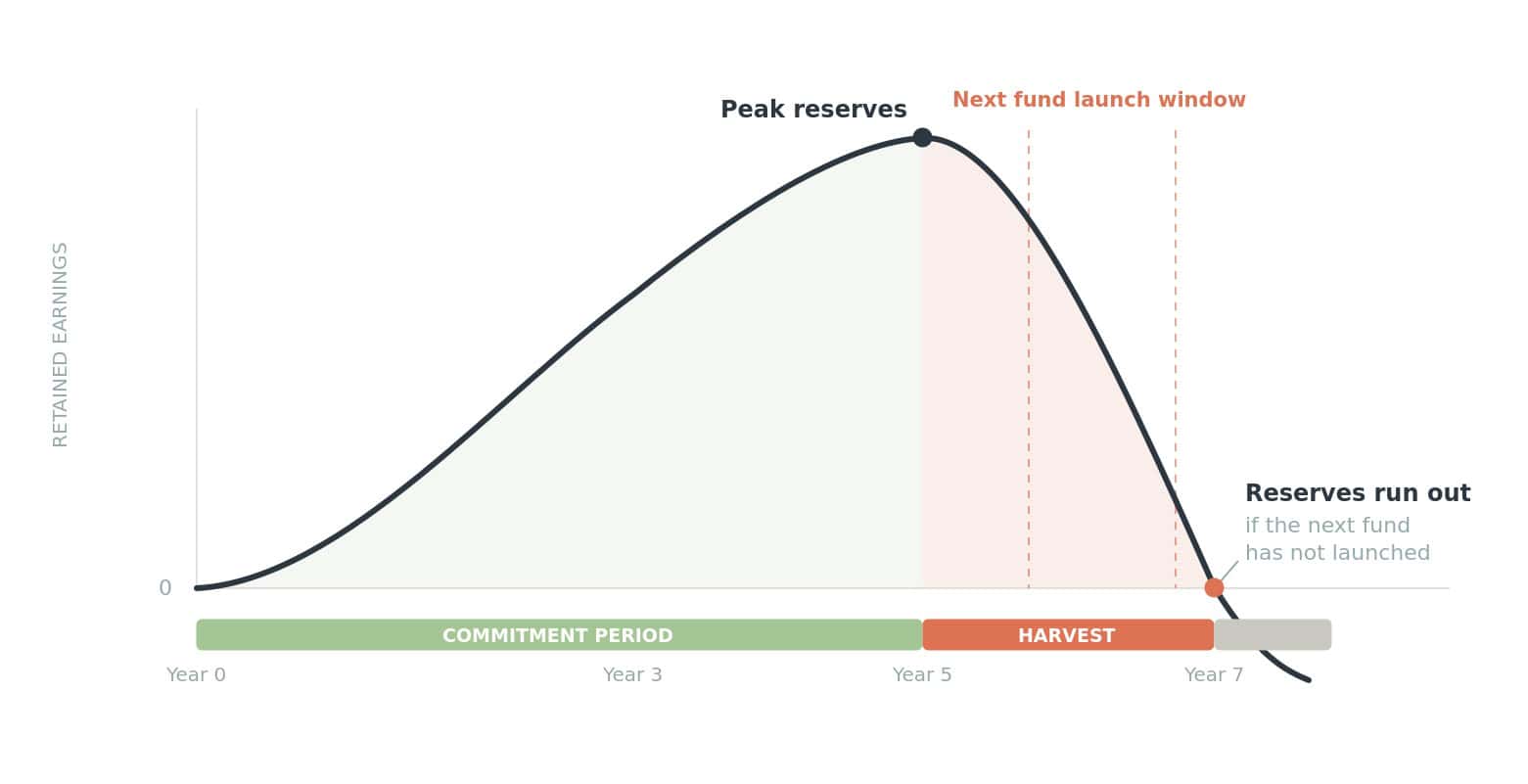

For the first few years, the management fees come in steadily and the business does well. Money builds up in the bank, and it is easy to mistake this stretch for the normal state of things. It is the good part, and the good part does not last.

Then the fees drop. It usually happens around five years in, or once most of the fund has been invested. The exact trigger is written into the agreement with investors. Whenever it lands, the income falls, sometimes by a lot.

From there, the business lives off the money it put away earlier. The team still needs paying. The rent still needs covering. So the reserves start going down, and the business begins to run at a loss. This is the second half of the cycle working as it should, planned for and completely normal.

There is even an upside hiding in those lean years. The losses the business runs are not wasted. They build into something that pays back the day the next fund arrives, and that, as it turns out, is the thing the whole cycle hangs on.

Which leaves the one question that catches people out. The reserves do not last forever. There is a point where they run out. The next fund has to be up and running before that happens, and since raising a fund takes the better part of two years from first conversation to first cheque, the work on it starts today, counted backwards from the day the money runs out.

It comes down to the next fund

Strip it right back and two things decide when the next fund has to launch, and they point the same way.

The first is the runway. How long the money in the bank lasts once the fees have dropped. It is the reserve that carries the whole harvest phase, and it sets the clock. When it is gone, it is gone.

The second is the assessed loss. The losses the business runs in the harvest years build up and carry forward, and they can be set against the income of the next fund. That lowers the tax the business pays just as the new fees start coming in, so the relief lands right when cash is at its tightest. It is real money.

But it is money that only exists if there is a next fund to claim it. An assessed loss with nothing to set it against is worth nothing. And the runway only matters because something has to be up and running before it ends. A fund manager that never launches its next fund runs out of road, and the unused assessed loss goes down with it.

So the whole thing folds into a single question. Not only when the next fund should launch, but whether there is going to be one at all, and whether it is up and running while the reserves can still carry the gap. Get that right and the rest follows. Get it wrong, and nothing else you did will save the business.

What good actually looks like

This comes down to one thing: books set up to answer a fund manager’s questions instead of general small-business ones.

The difference is mostly in how things are grouped. A standard set of books lists costs the way the software spat them out. Salaries here, rent there, subscriptions somewhere else, all in one long list. It is accurate, and it tells you almost nothing. It shows what was spent. It says nothing about the business you are actually running.

The same accounts, just grouped. Nothing added, nothing removed. The costs simply sit where a fund manager would look for them.

Group the same numbers the way a fund manager works, and the picture changes. Income gets split so you can see where it comes from and what happens to it when the fees drop. Costs get sorted into the things that matter for a fund manager: the team, compliance and audit, the cost of doing deals, the office and the systems. Nothing new gets added. It is the same money, broken into the core mechanics of the business and read in the language a fund manager already thinks in.

Once that is done, the reports start to read like the business. The runway becomes a line you can see coming, years out. The tax becomes something you plan around. And the whole thing starts answering the questions you actually lie awake thinking about.

What this looks like in practice. The fund managers who run this well keep it simple. They set the business up from the start to think like a fund manager. They can see their runway years out. They treat the tax side as a plan rather than a year-end surprise. And when the question of the next fund comes up, they answer it from the numbers, not from a gut feel. That is the difference between hoping the money lasts and having a grounded view of how long it will.

Read how we helped redefine the finance function for a Dutch investment manager

The questions we keep coming back to

None of this depends on being big or complicated. If anything, it matters most when the business is lean, because that is when a misread runway or a missed tax saving is felt the hardest.

When we sit with a fund manager, the conversation tends to circle back to the same few questions. We find them more useful than any rule.

Which year does the money run out, on the current plan? If that is a feeling rather than a date, it is usually the first thing worth pinning down.

Is the fee step-down the anchor of the plan, or an afterthought? Everything before it builds reserves, everything after spends them, and it is easy to plan as though the shift is not coming.

What do the good-year decisions cost in runway later? Pay, hiring, how much you take out: they rarely feel like next-fund decisions at the time, but that is what they are.

Is the business behind the fund getting the same attention as the fund itself? One is what investors judge you on. The other is what keeps you around to raise the next one.

What we think finance is really for

Tidier reports are a nice by-product. What matters is being able to answer the question a founder actually worries about. Can we afford to grow the team through the lean years? When do we need to be out raising again? What does it cost us, in runway, to pay ourselves a bit more now?

Those are the questions that actually run the business, and you can only answer them well if the bookkeeping underneath was built to answer them in the first place. That is the whole idea. A finance team that takes what happened last quarter and turns it into a view on the decision sitting in front of you.

Most fund managers can tell you their IRR. The best ones can tell you their runway too.